|

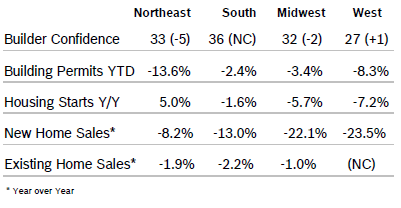

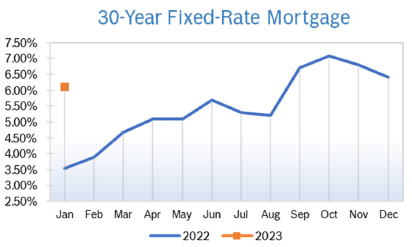

Builder Confidence Rises to 35 Builder Confidence rose four points to 35 in January after falling to 31 in December, according to the National Association of Home Builders/Wells Fargo Housing Market Index (HMI). The modest increase broke a 12-month string of monthly declines and came after interest rates fell slightly. The index hit an all-time high of 90 in November 2021. All three HMI indices posted gains for the first time since December 2021. The HMI index gauging current sales conditions rose four points to 40, the component charting sales expectations in the next six months increased two points to 37 and the gauge measuring traffic of prospective buyers increased three points to 23. NAHB says the increase points to a rebound in home building later in the year. Regional scores were mixed. Any number over 50 indicates that more builders view the component as good than view it as poor. Building Permits Fall 1.6% Overall building permits fell 1.6% in December to a 1.33 million unit annualized pace after falling to a downwardly revised pace in November. Single-family permits dropped 6.5% in December to 730,000 units after falling to 781,000 in November and were down 34.7% from December 2021. It was the ninth consecutive month single-family permits declined. Multifamily permits rose 5.3% to an annualized pace of 600,000 units after falling to a downwardly revised pace in November. Permits were down year to date in all regions. Housing Starts Fall 1.4% Housing starts fell 1.4% in December to a seasonally adjusted annual rate of 1.38 million units after falling to 1.43 million units in November. Single-family starts rebounded, rising 11.3% to a seasonally adjusted annual rate of 909,000 units after falling to 828,000 units in November. Single-family starts were down 25% from December 2021. Multifamily starts plummeted 19% to 473,000 units after rising to 599,000 units in November. Regional starts were mixed. Housing Starts Fall 3% in 2022 Total housing starts for 2022 dropped 3% from the 1.60 million starts recorded in 2021. Single-family starts in 2022 totaled 1.01 million, down 10.6% from the previous year. Multifamily starts in 2022 were up 14.5% compared to the previous year and exceeded a 500,000 annual pace for the first time since the Great Recession. New Home Sales Rise 2.3% New home sales rose 2.3% in December to a seasonally adjusted annual rate of 616,000 new homes from a downwardly revised rate in November. New home sales were down 16.4% in 2022 compared to 2021. The median price of a new home in December was $442,100, down 3.7% from November but up 7.8% compared to 2022, primarily due to higher construction costs. New single-family home inventory remained elevated at a 9 months’ supply. Around a 6 months’ supply is considered balanced. The number of homes available for sale was up 18.5% from December 2021 to 461,000. A year ago, there were just 33,000 completed, ready to occupy homes available for sale. By December 2022, that number increased 115% to 71,000, reflecting flagging demand and more standing inventory due to lower sales. New home sales were down in all regions. Sales of new homes are tabulated when contracts are signed and are considered a more timely barometer of the housing market than purchases of previously owned homes, which are calculated when a contract closes. Existing Home Sales Fall 1.5% Existing home sales fell 1.5% in December to a seasonally adjusted annual rate of 4.02 million units after falling to 4.43 million units in November, according to the National Association of Realtors. The decline was less than expected as dropping mortgage rates brought buyers off the sidelines, but it was still the eleventh consecutive month existing home sales fell. Sales were down 34.0% from December 2021. The inventory of unsold existing homes declined for the fifth consecutive month, falling to 970,000 homes, a 2.9 months’ supply at the current sales pace, down from 3.3 months in November but up from 1.7 months in December 2021.The median existing home price for all housing types in December was $366,900, an increase of 2.3% from December 2021, as prices rose in all regions. That marked 130 consecutive months of year-over-year home price increases, the longest running streak on record. Properties remained on the market for an average of 26 days in October, up from 24 days in November. Regional sales were mixed. Regional Housing Data  Mortgage Rates Fall to 6.1%

© Robert Bosch Tool Corporation. All rights reserved, no copying or reproducing is permitted without prior written approval.

|

|