|

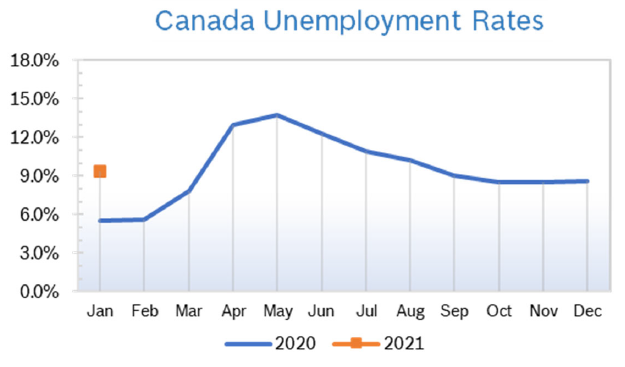

Unemployment Rises to 7.8%

Statistics Canada Limits Data Statistics Canada announced they will cut back on the number of reports they produce so they can focus on critical data in light of the CV19 outbreak. They will continue to publish the monthly Labour Force Survey, GDP, merchandise trade and inflation, among others. Some analysts pointed out that many of the economic reports come with a lag of several weeks or even months, and that experts trying to deal with the impact of CV19 are looking for real-time information. Consumer Confidence Falls to 88.6 The Index of Consumer Confidence fell 32 points in March to 89 after rising to 121 in February, according to the Conference Board of Canada. The reading came out March 19, with attitudes heavily impacted by fears surrounding the CV19 pandemic, as well as the sharp drop in oil prices. Canadians are worried about their jobs, their health and their economic future. The monthly Index of Consumer Confidence is constructed from responses to four attitudinal questions posed to a random sample of Canadian households. Consumer Prices Rise 2.2% The Consumer Price Index (CPI) rose 2.2% in February after rising 2.4% in January, according to Statistics Canada. Excluding gasoline, the index was up 2.0% year over year for the second consecutive month. On a seasonally adjusted monthly basis the index rose 0.1% in February, matching January’s increase. Year-over-year price growth for consumer goods slowed to 2.1% in February from 3.1% in January, while consumers paid more for services in February (+2.2%) than in January (+1.8%). January GDP Rises 0.1% Real GDP edged up 0.1% in January, as inclement weather in many parts of the country, automotive plant closures and labour unrest in the Ontario education sector partly offset growth in many sectors. Overall, 12 out of 20 sectors increased in January. Retail trade decreased 0.4% in January as 8 of 12 subsectors declined. A number of significant and record-breaking snowstorms affecting Newfoundland and Labrador, Southern Ontario and British Columbia's Lower Mainland played a part in the lower retailing activity in January. Construction was up 0.2% in January. Non-residential construction increased 1.7%, while residential construction edged up 0.1%. Statistics Canada posted this in the GDP release, which came out on March 31: “While the landscape of the Canadian and world economy has shifted since January, data from the beginning of the year are important in monitoring when and where changes occur over the following months. As such, this release and the detailed industry summary serves as a baseline of the Canadian economy for measuring the impact of the COCOVID-19 outbreak on various industries in the coming months.” Conference Board Trims Outlook The Conference Board of Canada issued an update the end of March, and now expects business investment and exports to post substantial declines and consumer spending to ease. As a result, economic growth will contract by a projected 2.7% in the second quarter. However, growth should resume in the third quarter, allowing the economy to avoid a technical recession. The Conference Board said there were huge downside risks to their outlook due to the unpredictability of the pandemic. Overall, they expect growth of just 0.3% in 2020 followed by a rebound to 2.5% growth in 2021. Bank of Canada Cuts Rates The Bank of Canada cut its key interest rate by another half-percentage point to 0.25% at the end of March, matching its all-time low. The bank also announced two new programs: a guarantee that it will purchase a minimum of $5 billion of Government of Canada bonds every week to assure liquidity and shore up the debt market and a package of benefits for small business. In addition, Prime Minister Justin Trudeau has asked banks and credit card companies to lower interest rates so Canadians can rely on borrowing to cover their expenses. Mortgage Applications Rise After the Bank of Canada (BoC) first cut interest rates from 1.75% to 1.25% in early March, mortgage brokers were inundated with requests for new loans, refinancing, preapprovals, renewals and demands to break current mortgages. The most popular type of mortgage in Canada is the five-year fixed-rate loan, which fell to as low as 2.29%, very close to the record low of 2.09% offered in November 2016 after oil prices crashed. It is also becoming easier for borrowers to qualify for a mortgage, with the federal government tweaking mortgage rules to be more responsive to the mortgage rate. Housing and Construction News Housing starts fell 1.9% in February to a seasonally adjusted annual rate of 210,069 units after rising to 213,224 units in January, according to Canada Mortgage and Housing Corp. (CMHC). The downward trend was driven by a decline in multi-unit starts. Multiple urban starts decreased by 6.1% to 146,072 units in February while single-detached urban starts increased by 11.9% to 53,232 units. Rural starts were estimated at a seasonally adjusted annual rate of 10,765. Canada’s home sales rose 11.5% in January to the highest level in 12 years, according to the Canadian Real Estate Association (CREA). Seasonally adjusted sales fell to 2.9% from December 2019, due primarily to an 18% drop in sales in the Lower Mainland of British Columbia. The actual average price for homes sold in January was up 11.2% from January 2019 to $504,350. Removing the pricey areas of Greater Vancouver and Greater Toronto, the national average price was around $395,000. Mortgage rates fell amid a sharp drop in bond yields with 5-year rates dropping to 4.99% from 5.34% and special rates, which are actually closer to what most buyers pay, falling to 3.1% from 3.2%. There is a lot of pressure on banks to cut rates even more based on current market conditions and sluggish growth prospects. Canadian inventory was very short prior to the outbreak, so buyers are tempted to disregard stay home and social distancing orders and to go out and see what is available. Some realtors are only helping clients who are in extraordinary circumstances. In addition, a host of provisions have been implemented to keep realtors, buyers and homeowners safe. Retail Sales Rise 0.4% Retail sales rose 0.4% in January to $52.0 billion after being virtually unchanged at $51.6 billion in December. The increase in sales was primarily attributable to higher sales at motor vehicle and parts dealers and gasoline stations, both of which were down in December. The other nine subsectors, which comprise the core retail sector, collectively declined 0.3%. Sales were up in 4 of the 11 subsectors, representing 48% of retail trade. After removing the effects of price changes, retail sales in volume terms decreased 0.3%. Sales at building material and garden equipment and supplies dealer fell 1.6% in January after rising an upwardly revised 4.1% in December. Sales were up in eight provinces, but dropped in Ontario. On an unadjusted basis, retail ecommerce sales were $1.7 billion in January, accounting for 3.7% of total retail trade. On a year-over-year basis, retail ecommerce increased 9.8%, while total unadjusted retail sales rose 3.9%. Retail Notes Greg Hicks is the new CEO of Canadian Tire. He was most recently president of Canadian Tire Retail, the company’s largest business, with more than $9 billion in revenue. Chairman Maureen Sabia said that Hicks’ appointment followed a rigorous global search that considered a number of both internal and external candidates. She said that Hicks is a world-class leader with a very strategic mindset and a proven ability to build high-performing teams and deliver exceptional results. He is also currently the chair of the Retail Council of Canada, and was previously responsible for the management of the company’s Pacific Rim offices in Asia. Current CEO Stephen Whetmore will serve as an advisor through the remainder of the year. © Robert Bosch Tool Corporation. All rights reserved, no copying or reproducing is permitted without prior written approval.

|

Archives

July 2024

|